My Thoughts on Bilibili ($BILI)

The bull case is a $200B+ business by 2030.

I’m not going to give an overview of Bilibili in this post — if you want that, check out this writeup by Lillian Li and read the company’s 20-F or F-1 filing. Lillian describes it as the result if “YouTube, Twitch, Steam, Patreon, TokyoPop and Netflix had a CRISPR-baby” — because, really, Bilibili is some combination of all of those things. But in this post, I’m going to assume you already knew that, and I’m going to focus on the investment case.

The first thing I want to say is that the Chinese video market is brutally competitive. There are players armed with large amounts of capital across every segment. Here is a brief overview:

Short video (<1 minute, similar to TikTok/Vine): Douyin (owned by Bytedance) and Kuaishou.

Mid-length (1-30 minutes, similar to YouTube): Bilibili and Xigua Video (owned by Bytedance).

Long-form video (30 minutes+, similar to Netflix): iQiyi (partially owned by Baidu), Tencent Video, and Alibaba Youku.

Game streaming (similar to Twitch): Huya and DouYu (currently being forced to merge by majority shareholder Tencent).

General purpose livestreaming: YY.

Not all of these are publicly traded themselves (some are subsidiaries of publicly traded companies), but only three are clearly worth more than $15B: Douyin (generated $18B in revenue last year), Kuaishou (expected to IPO at a $50B+ valuation next year) and Bilibili (market cap of around $30B). This list also doesn’t include many other platforms that have come and gone in the last 10 years. So surviving in this market is hard, and the fact that Bilibili is one of the most valuable players is very impressive. Even more impressive when you think about who they competed against: Baidu, Alibaba, Tencent, Bytedance, and Kuaishou. In fact, it’s so impressive that both Alibaba AND Tencent invested in Bilibili — how often do Alibaba and Tencent co-invest in anything?

Another point I’d like to make that speaks to how impressive Bilibili’s accomplishments have been. After YouTube took off in the US, a bunch of companies started to try to create the “YouTube of China.” As Rui Ma explains: “all of the video sites in China that initially tried to go after the YouTube model (like Youku) all eventually became PGC (professional generated content) platforms, that is, they became Netflix, not YouTube.” Bilibili is really the only one that succeeded in a big way with the “YouTube of China” model — and it wasn’t for lack of trying on the part of BAT + Bytedance.

All of that being said, Bilibili is at a critical juncture. There are two paths they can go down: they can try to “own the function” of mid-length video and become the “YouTube of China”, or they can try to “own the user” and capture a significant majority of time spent on entertainment for their core, Gen Z audience. I’ll discuss both options in turn.

YouTube of China

First of all, the term “YouTube of China” is an oversimplification for Bilibili. A better term might be “mass market video product”, since Bilibili is already expanding outside of its core segment of mid-length video into longer form original content (a la Netflix) and live sporting events, like the League of Legends World Championship. However, for the purposes of estimation, I’ll use YouTube as a reference since it’s probably the closest Western comp to Bilibili.

So, if Bilibili can become the “YouTube of China”, meaning they are the go-to source for mid-length video clips for all demographics across China, how many MAUs does that translate into? YouTube has about 2 billion MAUs of about 3.7 billion Internet users ex-China. That’s 54% penetration. It’s projected that there will be about 1.4 billion Internet users in China by 2030. At the same penetration level as YouTube, that’s about 750 million MAUs.

The next question is, how much can you monetize against each MAU (in other words, what is the ARPU)? This is much harder to predict, because I don’t think Bilibili has fully figured out monetization for their specific genre of video. Bilibili currently uses a plethora of monetization methods: mobile games (and associated in-game spend), a cut of livestreaming “tips”, premium memberships (subscription), advertising, and e-commerce. Though mobile games are the largest segment right now, this is almost certain to change, and I really don’t think even Rui Chen could tell you exactly how they’ll monetize in 2030. They’ll figure it out as they go.

I think the best we can do right now is to try to range-bound it. The obvious approach is to try to use YouTube as a proxy. YouTube’s run-rate global ARPU is currently ~$10. However, YouTube is, in my opinion, both undermonetized and mismanaged. Their revenue is growing 30%+, and I’m fairly sure MAUs are growing nowhere near that fast. So, there is likely significant upside to that $10 number on the basis of improved monetization. As for mismanagement: YouTube’s creator tools are pathetic, the platform hasn’t evolved for years, and their lack of creativity in monetization (just ads + subscriptions) is stunning vs. Bilibili’s many monetization levers. Bilibili’s daily videos watched per MAU are also roughly double YouTube’s, when I last checked. On this basis, let’s double YouTube’s ARPU to get to $20 for Bilibili.

However, there’s another factor to consider. A user’s “monetizability” is driven by their spending power — no matter how you monetize, whether it is advertising, subscription, “tipping”, a user is worth less from a revenue perspective if they have less money. Currently, China’s GDP per capita is similar to global GDP per capita, but if we assume that China’s GDP per capita grows 6% per year for a decade, that’s an 80% cumulative increase in user value. Adding in some improvements in ML that allow for better monetization, it’s safe to assume that ARPU targets can double over the next decade, to $40.

That’s one way of looking at it, but I mentioned that YouTube is mismanaged and undermonetized, so let’s look for a comp that is better managed and monetized: Facebook. Facebook’s global ARPU is around $30. Douyin’s current advertising ARPU is around $25, so this is a sensible ballpark for what Chinese ARPU could look like if Facebook operated there. Doubling as we did before to account for growth over the next decade gets us to a $60 ARPU.

Since we’re being hand-wavy, let’s average these together to get a 2030 ARPU estimate for Bilibili: $50. At 750m MAUs, that’s a $37.5B revenue opportunity.

Figuring out Bilibili’s margin profile at-scale is hard because each of their revenue streams has a different margin profile. For example, ads likely have 80%+ gross margins, game publishing margins for non-self developed games are probably closer to 40%, and margins on premium memberships, which primarily provide early/exclusive access to original content, are probably close to 0% right now as the company has alluded to premium memberships “covering the cost of original content”. The blended margin profile in 2030 will depend on the exact mix of the various revenue streams. That being said, YouTube’s gross margin is likely around 40%, since they split ad revenue 45/55 in favor of the content creator, and Netflix’s gross margin is also close to 40%. Let’s assume Bilibili’s gross margin at scale is 40% and operating margin is 25% (GM was 23.9% in most recent Q). That would equate to about $9.4B in EBIT, which yields a $188B market cap at a 20x multiple, in 2030.

So how can Bilibili move towards this “YouTube of China” vision? Well, they’re already starting to do it. Bilibili began as a primarily Anime, Comics, and Games (ACG)-focused video platform. They are now rapidly expanding into lifestyle (#1 category) and educational (#5 category) videos. Their recent investment in Huanxi Media (leading TV/movie studio) is another example of this content area expansion: in reference to the deal, Bilibili’s COO said “we are actively broadening and diversifying our content to appeal to a wider audience.”

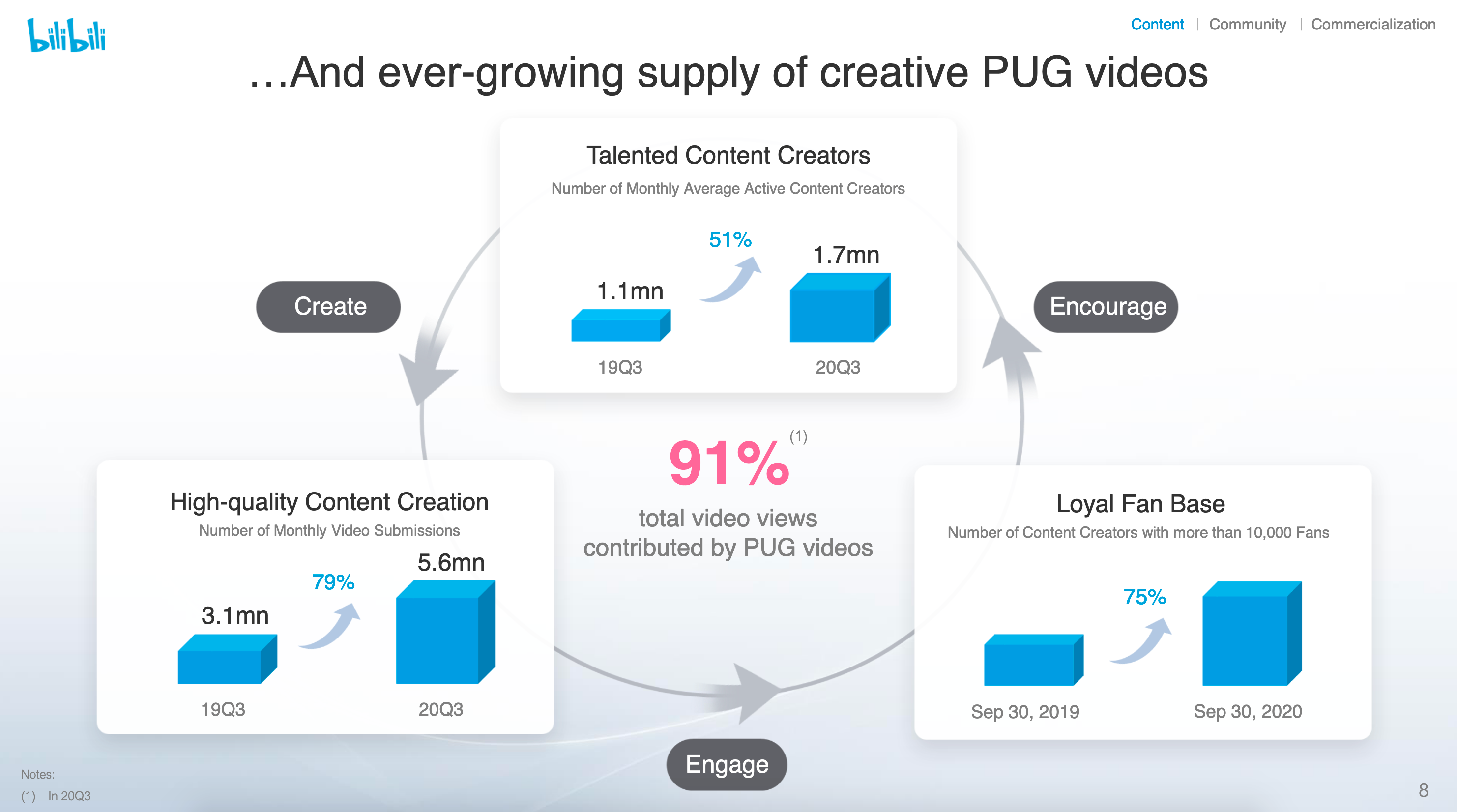

Furthermore, Bilibili is expanding its creator base, which is key to increasing the diversity of PUGC (professional user generated content) on the site, and in turn, the diversity of users. In Q3 2020, Bilibili had 1.7m monthly active content creators, up 51% y/y. Importantly, the number of content creators with 10k+ fans is up 75% y/y, so it’s not just the top creators who are pumping out the most-watched videos — which again, means more diversity of content and more diversity of users.

Most sell-side estimates target Bilibili at 400m MAUs in 2025, which is larger than China’s Gen Z population, which is estimated to be around 330m (and sell-side estimates are often a way for management to convey to the market its expectations, without setting explicit guidance — so while I don’t use sell-side PTs, I do look at their financial models). CEO Rui Chen has also said in interviews that he thinks the site can hold 500m MAUs, and management seems to emphasize the user growth runway on every earnings call. Clearly, Bilibili’s end-goal is not to be just a site for young anime fans.

Risks/counterpoints:

Bilibili’s engagement metrics are worse than those of Douyin and Facebook. DAU/MAU is <30%, vs. 50%+ for those platforms. Thus, my ARPU targets might be aggressive. On the other hand, time spent per day for Bilibili is much better than Facebook, and comparable to that of Douyin. Douyin is also in the early stages of monetizing, so there is likely upside to its number as well.

Is the mid-length video format still even relevant? Won’t everyone just watch Douyin and Kuaishou videos? I don’t think so. Even as TikTok has taken the world by storm, YouTube has consistently remained the top free app on the iOS app store. There is a world of interesting content that can’t be crammed into a <1 minute, vertical video. Bytedance’s Xigua Video announced a few months ago that they are committing $300m to get more creators on their platform — they wouldn’t be doing this if they thought their Douyin would eat mid-length video for lunch.

Couldn’t Xigua Video beat Bilibili? It’s possible, but Bilibili has an early lead and momentum in its favor. Xigua Video is not a new product — it’s been around for years — and consistently lagged Bilibili the whole time.

Doesn’t Bilibili’s growth seem slow for its size? Douyin and Kuaishou were both growing faster when they were a similar size to Bilibili: is Bilibili hitting a TAM wall? I agree the growth rate is slower than I would have guessed. I think the bottleneck is content — to attract users outside of the ACG community, they need a broader range of content, which means they need a broader variety of creators. I expect that their user growth will move in lock-step with this content growth, which the company is jumpstarting by investing in non-ACG original content, like documentaries and reality TV.

A noted strength of Bilibili’s is its “community.” The community is known to be positive and kind (in contrast to most of the Internet) — how can Bilibili maintain this strength if it becomes a massive platform with 750m MAUs? Balancing growth & community is a fine line that Bilibili is going to have to walk. But Bilibili is well aware — they’ve invested heavily in content moderators and founder Yi Xu focuses his time on community development.

“Owning” Gen Z

Until this year, the narrative around Bilibili was that it was a platform for Gen Z users — young people born between 1990 and 2009, according to the company’s definition (this year, the narrative has shifted to “YouTube of China”, and the stock price has moved accordingly).

If Bilibili can “own” the Gen Z demo, what is that worth? First, to be clear, Gen Z LOVES Bilibili. I think something like 80% of Bilibili’s users are Gen Z, and they spend an average of 81 minutes per active user per day on the platform, and that doesn’t include the time they spend playing mobile games operated by Bilibili. For context, the average Snap DAU spends only 30 minutes on the app and the average Facebook user spends close to 40 minutes per day on the app. In fact, time spent per day on Bilibili is comparable to that of Douyin and Kuaishou, which are known for their addictiveness. All of this is to say that young people, which are probably the most attractive demo of users to have, are spending a lot of time on Bilibili every day. Even if Bilibili fails to meaningfully expand their base of users, if they expand their time share within Gen Z, that has to be pretty valuable on its own, right?

Though it’s going to be hand-wavy, I’ll try to range-bound this as well. There are 330m Gen Z’ers in China. If we assume they can monetize at $100 ARPU, that’s a $33B revenue opportunity.

There are a few reasons this is not as outlandish as it seems. On the MAU side, 330m is quite conservative. It does not include the ~150m people who will join Bilibili’s core 10-30 year old demographic over the next years. And with almost 200m MAUs right now (up from 130m at the end of 2019), Bilibili is already well on its way.

The ARPU target needs more defending: $100 may seem high, but so is the engagement for Bilibili’s most avid users. Serious ACG fans go to Bilibili conventions, buy merch, and identify personally with their love of ACG — similar to how hardcore sports identify with their teams here in the US. I didn’t focus on the community aspect as much in this writeup, but Bilibili is the primary online community for ACG fans in China — the 100 question quiz you have to pass to become an “official member” and the unique “bullet commentary” on videos are both reflections of this. Obviously, not all 330m Gen Z’ers are this serious about ACG, but the widespread interest in ACG across young people in China is I think difficult for people based in the US to understand (since ACG is more niche here). I really think ACG in China is much more akin to sports in the US — some people are really serious about it, but even those who aren’t will watch games on occasion and watch the Super Bowl every year.

A friend explained to me a lens through which to view Bilibili’s decision-making. They seem to make decisions based on “what would a 20-year-old in China who is somewhat anime-inclined like?” And this led in directions that seem to be orthogonal to a “YouTube of China” strategy — for example, publishing mobile games like Fate/Grand Order, building a dedicated comics app (Bilibili Comics), producing 40 Chinese Anime films/shows in 2020 and 2021, and paying for the rights to the League of Legends World Championships. Clearly, Bilibili wants to “own” this demographic, capturing as large a portion of their leisure time as possible. When viewed through that less, $100 ARPU doesn’t seem out of reach.

Using the same 25% operating margin assumption as above, this $33B revenue opportunity translates to a $165B business at a 20x EBIT multiple.

Risks/counterpoints:

Isn’t Gen Z fickle? Couldn’t they decide they want to use something else in a few years? Yes, it’s possible if Bilibili doesn’t continue to evolve its product (remember Vine?). It’s important to monitor key KPIs (below) for any signs of a slowdown.

Won’t Bilibili’s most hardcore ACG fans leave as the platform goes more mainstream? Again, it’s possible. There is some evidence this is already happening, but it doesn’t seem to be happening in significant numbers (yet). Watch to see if premium membership growth slows significantly, since the most die-hard fans tend to buy premium memberships.

Adding it all up

Bilibili doesn’t seem to have decided which of these strategies to pursue — rather, it seems like it’s going after both. I don’t think the two are mutually exclusive — Bilibili can be a platform that appeals to a broad swath of the population, and at the same time cater more specifically to a Gen Z, ACG-loving fan. That’s why I think the real bull case is some additive combination of the two. Obviously, there is overlap so the two can’t just be added together — nonetheless, I think the combination could yield a $200B+ business in a decade.

Quick note: you might be thinking, isn’t $188B + $165B way more than $200B? Yes, but there is huge overlap between the two. In fact, the second scenario may be largely integrated into the first — for example, the $100 ARPU power-users average with the once-a-month users to get to a $50 ARPU. I don’t what the exact extent of the overlap will be, and I don’t want to make large assumptions without basis, so I’m calling it $200B.

In both sections, I outlined the risks and counterpoints — the strategy and execution challenges are far from trivial. Furthermore, given how hand-wavy my projections are, they are liable to be off-base: my ARPU projections might be way too ambitious, and my margin structure assumptions are really just educated guesses. It’s also hard to predict the likelihood of these best-case scenarios actually occurring — I think they’re possible, but I don’t know the exact probability. I’d love to hear from others who are more familiar with Bilibili as to how they think about its future — please reach out!

P.S. KPIs to Track

There are two things that matter: how much time is spent in the app by users, and how well that time can be monetized.

Right now, and for the next few years, I think investors should focus on the former — as long as gross margins don’t decrease (meaning that Bilibili is not attracting users by paying huge sums for content and then offering it to users below cost). I’m focused on: MAUs, DAUs, time spent in app, number of premium memberships, and number of videos watched. The metrics that drive this are: number of creators on the platform and number of videos uploaded.

After a few years, investors should start tracking ARPU more closely. We should look for average revenue per MAU and average revenue per DAU to rise, and for gross margins to expand as well. We should also look for S&M spend to moderate significantly — at a certain level of scale and brand recognition, Bilibili shouldn’t need to spend much at all to acquire users.

Disclosure: I currently do not hold any shares of Bilibili. This is subject to change at any time, without notice. I run a concentrated personal portfolio, and I need to see a clear path to a 25% IRR over 5-10 years for all names in my book. I’m not there with Bilibili right now, but I spent so much time researching the company and found it so interesting that I felt I had to write about it anyway. And who knows, maybe someone who is a lot smarter on Bilibili than me will reach out and change my mind!

Acknowledgments: Thanks to Shantanu Jha for helping me understand Bilibili much better.

If you liked this article, follow me on Twitter, where I tweet about exciting businesses like Bilibili!

Nice article!