Hedge Fund Fees

Another illustration of the power of compounding... and why the best hedge fund managers are so rich.

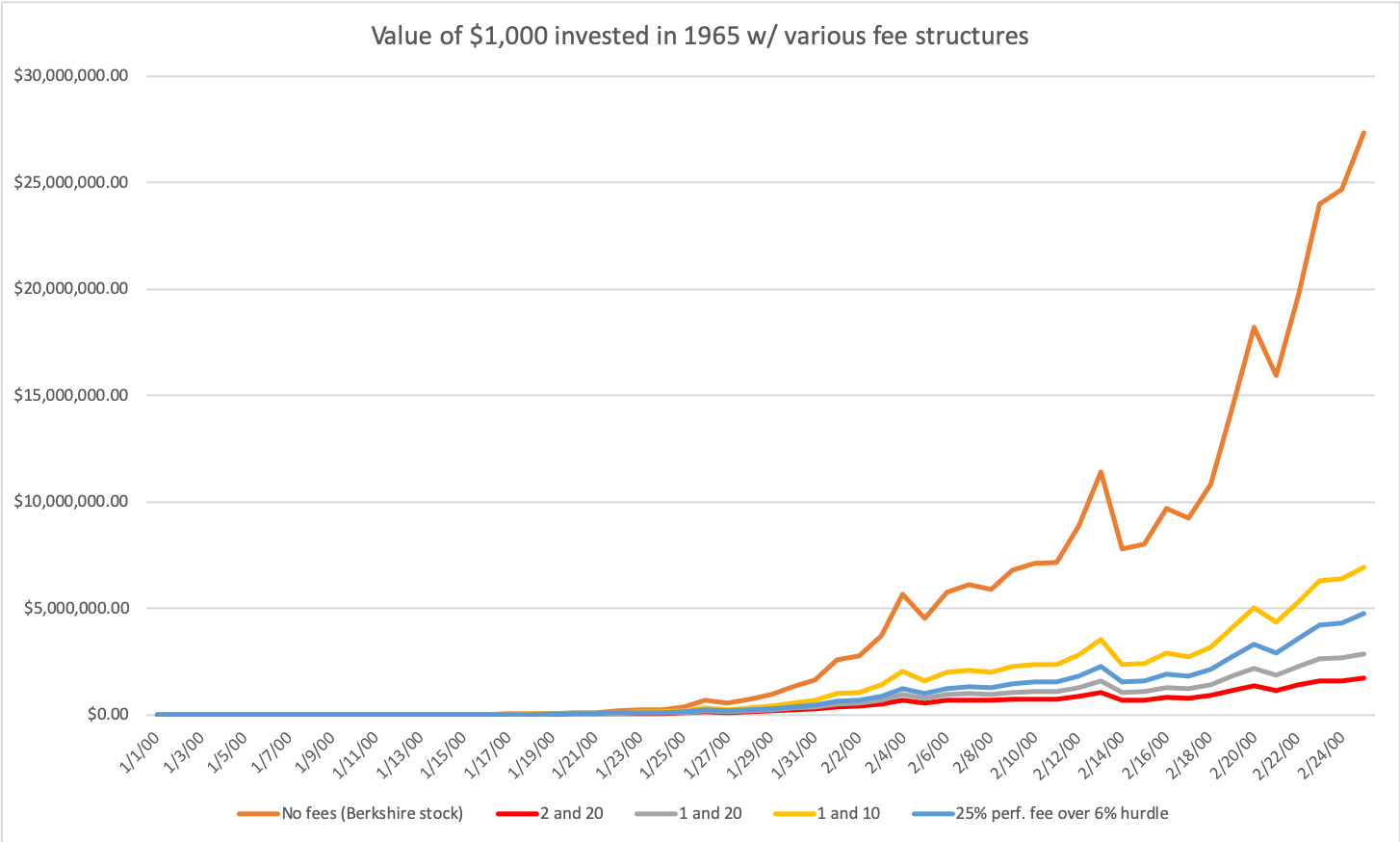

I was interested in seeing how different types of hedge fund fee structures affect the financial outcomes for the manager (general partner/GP) and investors (limited partners/LPs). To do so, I took Buffett’s Berkshire track record, and tracked what returns to investors would have looked like if, instead of running Berkshire, Buffett had continued running a hedge fund, with various different fee structures. The results are as follows:

2 and 20:

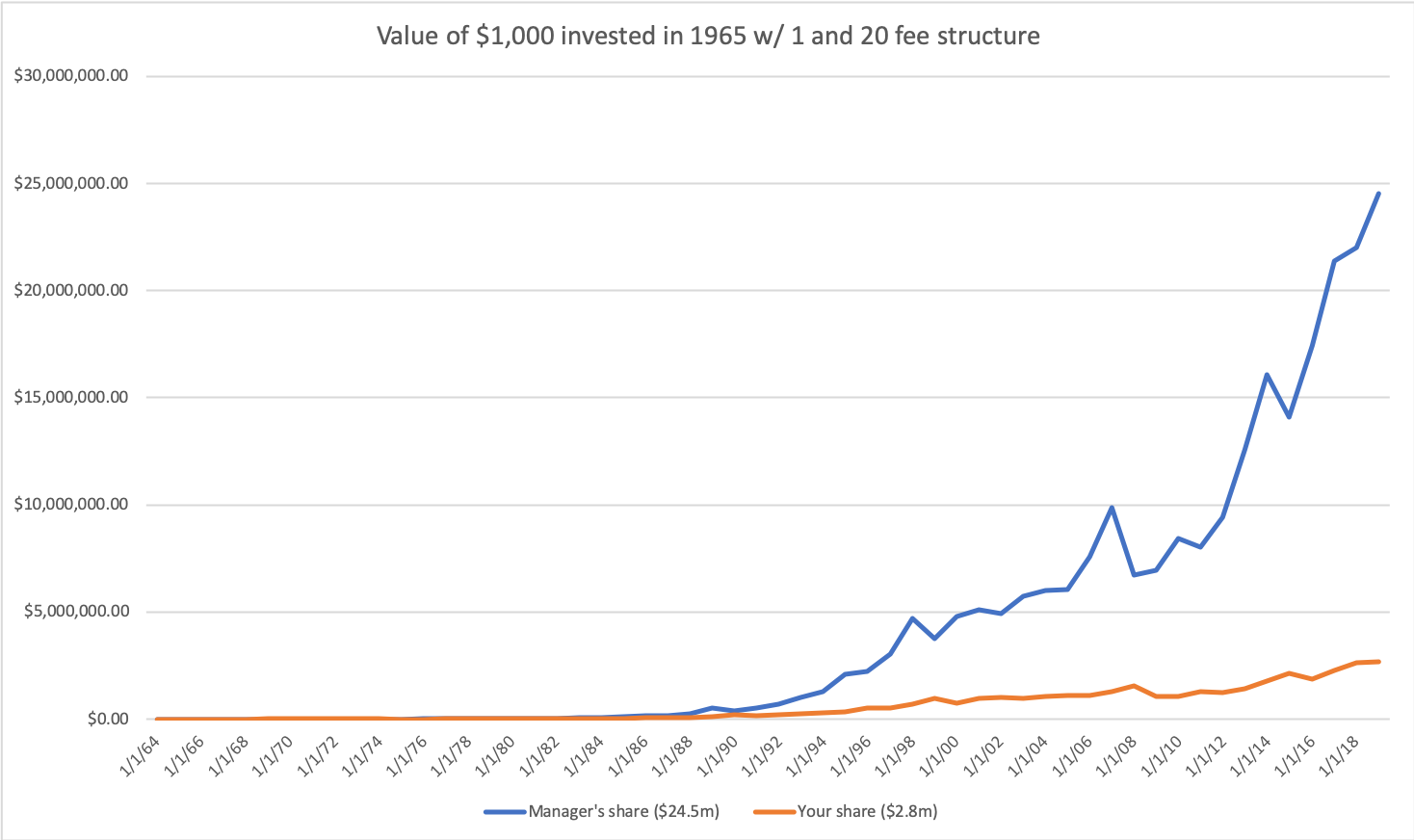

1 and 20:

1 and 10:

25% of profits over a 6% hurdle rate, with no management fee (the fee structure of the actual Buffett Partnership):

Isn’t it SHOCKING how much of the economics accrue to the manager, no matter which fee structure is utilized? To drive the point home, here’s a graph of your account value as the investor, under the various fee structures:

I consider myself fairly familiar with the hedge fund industry and I had no idea how good the economics can be over a long period of time. To be clear, this only works if you’re actually able to generate above-average returns for a long period of time, like Buffett. If you can’t… no fee structure is going to save you – and you have no business being an investor in the first place. But imagine how wealthy Buffett would have been if he just kept running the hedge fund instead of minting money for all these public shareholders for free…

Anyways, that’s all I wanted to share: yet another example of the power of compounding at work.

P.S. A few technical notes:

All of these calculations assume a high water mark is utilized.

I calculated management fees based on the average of the previous and current year’s balance, not the year end balance. This is because management fees are usually assessed quarterly or monthly in arrears, not once at year end.

Performance fees are calculated based on pre-management fee year end account value.

I assume the manager reinvests all fee income back into the fund. I do not account for expenses (travel, audit, compliance, staff, expert networks, data, etc.) that would come out of the fees prior to reinvestment.

I do not factor in taxes, for either the LP or the GP.

I really enjoyed the simplicity of the thesis. Too many pitches “report” instead of providing variant “insights.” I look forward to more of your material!