Airlines, Part I

Airlines, Part I

Is there value in everyone's "favorite" industry?

Lufthansa aircraft idled in Berlin in response to COVID-19 flight cancellations

Given the market carnage that COVID-19 has wrought upon anything in the travel and entertainment space, I thought it would be particularly relevant to do a series of posts on airlines and how they’ve been impacted. This post will lay the groundwork.

In investing circles, the airline industry is well-known as a graveyard. Hence the famous joke: “How do you become a millionaire? Become a billionaire, and then invest in an airline.” The general reasons are well-known: airlines are a cyclical, high fixed cost, capital intensive, commodity industry with low barriers to entry. The industry as a whole tends to go through cycles (like a lot of commodity industries): profitable years result in capacity expansion (new airlines enter, existing airlines buy more planes) which results in oversupply (too many planes relative to passengers), which results in bankruptcies which reduces capacity, leading to profits — and the cycle repeats. Add in semi-random economic shocks like 9/11, the financial crisis, and COVID-19, and you have a money pit of an industry.

Even so, I decided to look into the space. I compiled a list of 51 large, publicly traded airlines, along with:

CAGR (compounded annual growth rate) of total shareholder return from 12/31/1999 to 3/31/2020

CAGR of total shareholder return from 12/31/2006 to 3/31/2020

I specifically included Q1 of 2020 to ensure the impact of COVID-19 was accounted for.

Source: S&P CapitalIQ

A few notes:

This list sorted by CAGR from 12/31/1999 to 3/31/2020.

Only 18 of the 51 airlines (1) existed and were publicly traded in 1999 (2) did not merge or go bankrupt in the intervening years, which is why there are only 18 airlines in the table. Airlines like easyJet, Wizz Air, and AirAsia did not exist in 1999, and household names like United, American, and Delta went through bankruptcy in the intervening years.

6 of the 18 airlines listed beat the S&P over the 20-year period. This is not great, especially considering this list doesn’t include bankruptcies, as mentioned above. The real fraction of airlines that beat the S&P is much lower than 6 out of 18. These 6 are: Dart Group, Ryanair, Hawaiian, Southwest, Alaska, and China Southern.

I’ll give a bit of context into each of these airlines, before we study them in more depth.

Dart Group:

Several segments: Fowler Welch (distribution and logistics), Jet2.com (low-cost leisure-focused airline), and Jet2holidays (tour operator)

Founder and CEO Philip Meeson owns 32% of the company

Ryanair:

Europe’s largest low-cost carrier (and airline)

Led by CEO Michael O’Leary (quite a character, look him up), who owns a $500m+ stake in the airline

Expanded steadily in Europe over the years and flies only Boeing 737 aircraft

Hawaiian Airlines:

Underwent bankruptcy in 2003, but equity was not wiped out (which is why it is still on this list)

Bankruptcy process allowed for fleet restructuring, labor contract re-negotiation, etc. which gave it a leg up afterwards

Full-service carrier doing inter-island travel between the Hawaiian Islands as well as long-haul travel from Hawaii to destinations in Asia, Australia, and North America

Southwest Airlines:

Founded by Herb Kelleher and began operations in Texas in 1971

Largest low-cost carrier in the world today, and the most financially successful airline in history (see stock performance since 1978 IPO)

Has been profitable for 47 consecutive years (underheard of in airline industry)

Pioneered the low-cost carrier (LCC) model, which includes: a short-haul point-to-point network, “no frills” offering (focus on low fares), use of secondary airports with lower congestion and fees (Dallas Love Field, Chicago Midway), high aircraft utilization (famous 10-minute turnaround), fleet standardization to reduce maintenance expense (all Boeing 737 fleet), high density (lots of seats on aircraft), and direct distribution (all tickets booked through Southwest.com, cutting out travel agents)

Alaska Airlines:

Like Southwest, one of the few U.S. airlines to avoid bankruptcy in the 2000s

Unlike Southwest, lost money in 7 of the 9 years between 2000 and 2008 (inclusive)

Standardized on Boeing 737 fleet in 2000s under CEO Bill Ayer

China Southern Airlines:

One of China’s “big three” state-owned airlines

Not particularly efficient or competitive, and probably would have gone bankrupt a long time ago if it was a private company

Received repeated capital injections from Beijing (2008, 2010 are examples)

U.S. airlines note: In the 2000/early 2010s, most major U.S. airlines went bankrupt (9/11 and high jet fuel prices are some of the common reasons given). This led to industry restructuring as Delta and Northwest, United and Continental, and American and US Airways combined. After this consolidation, capacity rationalized (i.e. airlines stopped buying unnecessary planes) and the entire U.S. airline industry was enormously profitable for much of the 2010s – until, of course, COVID-19. We’ll cover consolidation in more depth in a later post, but the key takeaway is that all U.S. carriers (largely regardless of efficiency) performed well in the 2010s, so their results should not be directly compared to those of carriers from other regions of the world where such consolidation has not (yet?) occurred.

In this analysis, we are looking for “compounders”, which are airlines that have shown a consistent ability to earn above their cost of capital, regardless of industry operating environment. For this reason, we will exclude Hawaiian, Alaska, and China Southern. Hawaiian went through bankruptcy, Alaska really only performed well after U.S. consolidation, and China Southern has been coddled by the state. Thus, we’ll focus on Dart, Ryanair, and Southwest, which have performed regardless of operating environment.

Let’s take a step back here. We are now left with only 3 airlines, out of the numerous publicly traded airlines that existed in 1999. The vast majority of airlines either went bankrupt or underperformed. This shows that airlines are probably not the “best pond to fish in” when it comes to long-term value creation.

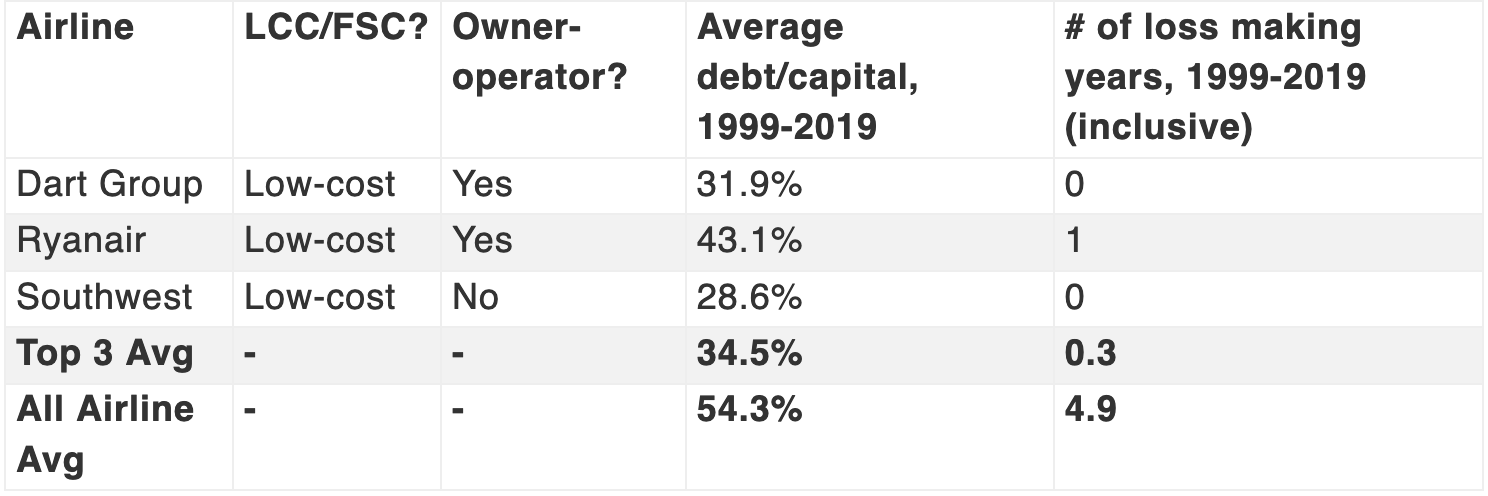

A few key observations:

All three are low-cost carriers

2 of the 3 are owner-operated, and Southwest’s founder Herb Kelleher was CEO until 1998 (his cultural impact on the company lasts to this day)

All three use below-average amounts of leverage

All three rarely, if ever, lost money

These airlines did not outperform by levering up and swinging for the fences, making big profits in good times and taking huge losses in bad times. They’ve been consistently profitable and are conservatively financed, and they show that although it is difficult, it is possible to rise above the boom-bust cycles of the industry. This is an important insight because it shows that even in an industry that has bad economic characteristics, the right management team and operating philosophy can make all the difference.

This post is getting long, so I’ll leave it at that right now. This post will be the first of a series on the airline industry, and in future posts, I plan to do the following:

Dive deeper into Dart, Ryanair, and Southwest, and the low-cost carrier model globally

Explore the U.S. airline industry consolidation argument. This is the argument that the U.S. airline industry has permanently exited the boom-bust cycle due to consolidation and is reportedly what led Warren Buffett to take large stakes in United, Delta, American, and Southwest in 2016 after criticizing the industry for years

Explore the impact of COVID-19 on airlines moving forward